Decoding Health Insurance: Deductibles, Copays, and Out-of-Pocket Maximums

Key Takeaways

- A deductible is the amount you pay before insurance contributes to covered healthcare expenses.

- Copays and coinsurance involve sharing the costs of care with your insurer after you meet the deductible.

- The out-of-pocket maximum places a yearly cap on the amount you spend for covered services, offering financial protection.

- Choosing the right plan means understanding these components and how they impact your care and budget.

Health insurance can be difficult to navigate with its unfamiliar terms, dense paperwork, and complex coverage guidelines. Understanding a few essential principles will help you make confident, cost-effective choices from the start. Concepts like deductibles, copays, and out-of-pocket maximums determine how much you pay before insurance kicks in and how your ongoing healthcare bills are managed. When you or a family member is seeking specialized options like CHAMPVA dental, this knowledge becomes even more valuable, as dental plans often mirror medical insurance with their own rules about what you owe.

Knowing the difference between what is covered, your share of costs, and what counts toward your yearly limits can shield you from unwelcome surprises at the doctor’s or pharmacy. Most everyday health plans work similarly, but it’s wise to check your details carefully or ask your benefits administrator to clarify them before scheduling major appointments or procedures.

These terms may sound technical, but they affect how quickly your financial obligations shift from your pocket to your insurance plan. When you understand the details, you are better positioned to select protection that fits your health needs and keeps your spending under control.

What Is a Deductible?

A deductible is the set amount you pay for your own covered healthcare before your insurance company starts to contribute. Think of it as the first milestone in your annual health expenses. For example, if your deductible is $1,500, you will be responsible for covering the first $1,500 of your health services for the year, after which your insurer will begin to pay its share. Deductibles reset each plan year and can vary widely: lower monthly premium plans tend to carry higher deductibles, which is worth considering for those who anticipate frequent medical visits or treatments.

Understanding Copays

Copays are fixed dollar amounts you pay when you receive certain health services, such as seeing your primary doctor or filling a prescription. You might find, for instance, a $20 copay for specialist visits or a $15 copay for medications. Copays are usually separate from your deductible, meaning you owe them whether or not your deductible has yet been met. While copays do not reduce your deductible, they do count toward your total out-of-pocket maximum.

Coinsurance Explained

After your deductible is paid in full, coinsurance begins. This means you pay a set percentage of the covered service cost, and your insurance pays the rest. Most coinsurance arrangements are shown as two numbers, for example, 20/80. If you have met your deductible and require a $1,000 treatment, your 20 percent coinsurance would require you to pay $200, with the insurer covering the remaining $800. Coinsurance applies to each covered cost until you reach your annual maximum.

Out-of-Pocket Maximum: Your Financial Safety Net

The out-of-pocket maximum is the cap on what you will spend in a calendar year on covered health services. Once you have paid this amount through deductibles, copays, and coinsurance, your insurance pays for all additional covered care for the rest of the plan year. Premium payments and non-covered services do not count toward this limit. For 2025, the federal government has set individual out-of-pocket maximums at $9,200 and family out-of-pocket maximums at $18,400, according to resources on HealthCare.gov. Hitting your out-of-pocket maximum can offer relief from significant or unexpected medical bills, ensuring you do not face endless financial risk.

How These Elements Work Together

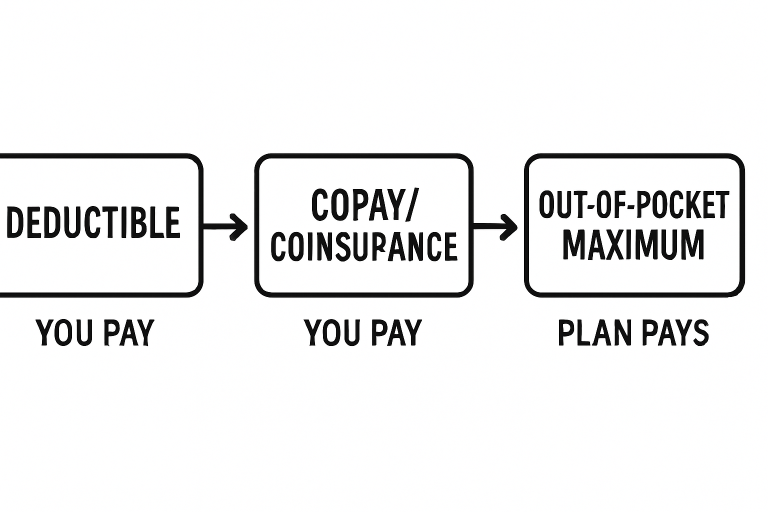

Deductibles, copays, coinsurance, and out-of-pocket maximums interact in a predictable order during your policy year. First, you pay the deductible, which is your entry ticket to having insurance begin sharing costs. After meeting the deductible, any further bills for covered services are calculated based on your plan’s copay or coinsurance requirements. All your eligible cost-sharing payments throughout the year push you closer to the out-of-pocket maximum. Once reached, the insurer takes on responsibility for 100 percent of covered medical bills, no matter how high.

- Paying the Deductible: You shoulder the full cost of covered services until you’ve paid your annual deductible.

- Entering Coinsurance: After the deductible is cleared, you and the insurance company split the bill based on your plan’s coinsurance rates, and copays may still apply for some services.

- Maxing Out-of-Pocket: When all your eligible payments reach the maximum limit, your plan begins paying 100% of covered health care costs for the remainder of the year.

Choosing the Right Plan

The right health insurance plan balances your regular health needs, risk tolerance, and financial comfort. Plans with lower premiums usually come with higher deductibles and larger out-of-pocket spending. These may be attractive if you are healthy and rarely visit the doctor, but if you expect high medical usage, a plan with a lower deductible, even with higher monthly payments, may save you money and stress in the long run. Always estimate your total yearly costs under several scenarios—such as managing chronic conditions or handling emergencies, so you can confidently choose a policy that fits your circumstances.

Final Thoughts

By learning how deductibles, copays, coinsurance, and out-of-pocket maximums work together, you reduce your risk of large unforeseen bills and get peace of mind knowing you are protected. Making your health insurance work for you starts with understanding these key concepts and comparing plans carefully each enrollment period.